Investment Outlook – Trend 8 , Published Mar 16, 2017

The introduction of the goods and services tax (GST) is a long-awaited and game changing tax reform, aimed to simplify and rationalise India’s indirect tax regime. The passage of the legislation by the parliament is a major milestone on the road to the introduction of the GST.

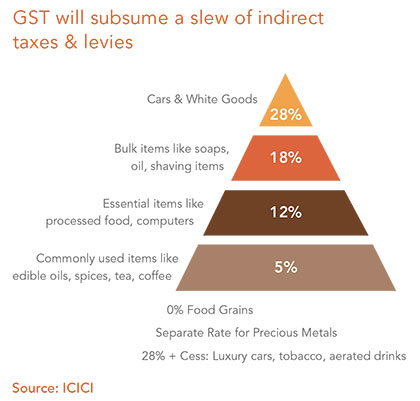

Structuring the GST

The tax reform is expected to be implemented from 1-Jul-17. This is likely to affect the growth-inflation dynamics as well as the ease of doing business.

Although India became a single country politically post-independence, it continues to operate as a collection of different markets in each state with different levies within and while moving between states. The GST is supposed to subsume a slew of indirect taxes and levies of the Central and State governments, with Central GST and State GST to be concurrently levied on both goods and services at the point of consumption. The GST will be levied on all goods and services, except petroleum products and liquor.

Proposed tax reform would shift trade from the unorganised to the organised segment and improve efficiency in the system.

A key highlight of the GST lies in the area of tax governance, where the current system is plagued with discretionary powers and coupled with ad-hoc tax levies. These lead to poor business perception. However, introduction of GST would move towards a transparent and stable tax regime and would create a common market with uniform tax rates across the country. The removal of the cascading effect of indirect tax rates across the States and Centre would dramatically improve the ease of doing business. Also, consequent significant reduction of product-wise exemptions would broaden the tax base and make the process of providing input tax credit more efficient. Since the GST would be a destination-based tax, the proposed 1% additional tax to be retained by producing states should minimise the impact.

Against the popular perception, it is unlikely to impact inflation adversely, as the proposed multiple slabs of rates are aligned with current levies. However, basis the global experience, over the longer term, it would boost economic activity substantially and improve the Government’s revenue base.

Since the proposed GST rate aligns with the revenue-neutral rate, the effective tax rate will come down, which will broadly offset the increase in tax base as the exemption list is also pruned down. However, GST will help reduce tax evasion, given the lower exemption list and resultantly improve compliance.

For the corporate sector, GST would bring several changes. Early enrolments could make it less disruptive than widely perceived. Grandfathering of the current location-wise tax benefits could be smoothened by one-time settlements and/or interest-free loans to the extent of amount of tax collected. Proposed tax reform could bring up four scenarios, impacting corporates:

As corporates transition to the new tax regime, they are likely to experience operational challenges in the shorter term. However, the long term benefits are likely to be tangible and sustainable and will aid in delivering productivity benefits and operating leverage.

Download ReportInvestment Outlook 2017