Nov 12, 2018

In investing, what is comfortable is rarely profitable – Arnott 1954A Holiday Gift for Investors

The rapid decline in crude oil prices is a direct boost for businesses and consumers, and particularly for India as a crude oil importer. Brent crude is at the lowest levels it’s been since May 2018, with prices down from a high of 86.74 to 70.08, or 19.2%, the drop driven by speculators exiting positions due to rising inventory builds and the U.S. relaxing of sanctions on Iranian oil imports for eight countries including India. This immediately improves prospects for an uptick in global demand, domestic demand and margins.

Gridlock in Washington a Gift for Investors

What’s clear from the U.S. midterm elections is that Trump’s trade war escalation, tax cuts and style of stewardship has not resonated with voters. Republicans voted Republican, Dems voted democrat and independents exercised traditional buyer’s remorse by turning the House over to the Democrats. For investors, gridlock in Washington was the best outcome.

Another Positive Surprise… Highest Equity Inflows This Year in October and Strong SIP +42% YoY

The consistent refrain that domestic investors would eventually capitulate and pull back on equities has not materialized. Despite massive selling this year by FIs – the largest selling since 2008 – the markets have held up far better due to strong support by the domestic investor. SIPs are now up to 7,900 crores a month, up 42% versus last year. Net inflows into equity MFs jumped to 14,780 cr. The story continues to appear structural in nature, as SIPs have risen consistently this year.

And Earnings Growth Has Recovered and Looking Solid

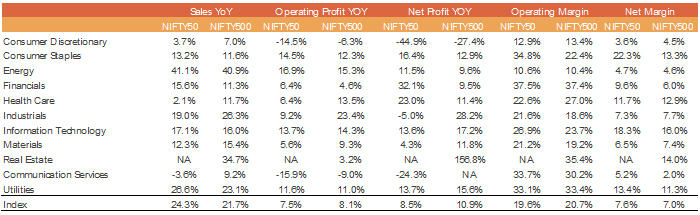

Earnings growth data for Q3 CY18 have been a bit of a roller coaster. We first reported healthy growth, which then tapered at around the half way mark. Now, with 345 companies reporting in the CNX 500, and 43 of 50 Nifty companies reporting, the performance is impressive. Adjusted for PSU bank losses, broader market earnings are up 19.4%.

Sales Are Up 24.3% for the Nifty 50 and 21.7% for the broader CNX 500, with 43 and 345 Companies Reporting…

…While Earnings Are Up 8.5% for the Nifty 50 and 10.9% for the CNX 500

Adjusted Earnings ex PSU Bank Losses and Reliance Telecom Losses…

…And Earnings for the Broader Market are Up a Healthier 19.4%

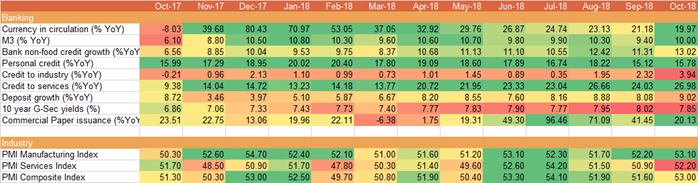

Credit Growth Hits a Five-Year High at 14.8%, Remains Healthy

In further good news on the credit growth front, concerns about slowing credit have not materialized. The concerns had centered around NBFCs and whether credit would be easily available to consumers. Credit growth for the month of September was 11.7% and rose to a near five year high of 14.8% for the fortnight ended October 26. Clearly, concerns about a liquidity freeze have not materialized; rather, the picture appears to be improving steadily. Much of the fresh credit growth is being driven by small-ticket retail loans. There has also been a slight pickup in activity on the corporate loan growth side. Yet again, a surprising data point.

Corporate Lenders Recovering

In additional positive developments, large corporate focused lenders that suffered rising NPAs for years are now showing signs of stabilizing. As a result of higher recoveries from bad loans and slowdown in new NPAs, as well as a clean-up of the books, provision write backs and improving asset quality, these banks look poised for better days ahead. However, risks remain, particularly with regards to lending to exposures to NBFCs, IL&FS and other debt laden entities.

For PSUs, Good and Bad News

The good news: the government expects four public sector banks (PSBs) to graduate from the Reserve Bank’s prompt corrective action framework based on their improved financial performance. Bank of India, Bank of Maharashtra and Corporation Bank are on the list. The bad news: ratings agency Crisil is out with a view that PSU banks will require a fresh equity infusion of Rs 1.2 lakh crore in the next five months. This estimate is Rs 21k crores higher than announced in Oct 2017, to meet Basel III capital norms.

Credit Growth & PMI Data Suggest the Economy Remained on Health Footing During October…

With only Rs 1.12 lakh crore infused over the past 18 months, another Rs 99k crore would be still needed by March 2019. The money is needed for the PSBs in the Prompt Corrective Action (PCA) framework of the RBI.

Meanwhile, a Funding Squeeze Is Being Felt by the Real Estate Sector

It’s not all good news however. The real estate sector is experiencing a funding crisis. In some cases, sanctioned home loans were not being disbursed and funds for construction linked schemes not being released last month. The caution has also led to a rise in home loan interest rates by 50-75 bps. Developer funding has become much tougher to come by, with rates blowing out by as much as 300 bps.

Outlook

Equities

Last fortnight, we made the case that the news is mostly in the price, and by measures such as market cap to GDP, and price to dividend yield, the market is approaching trough valuations. We suggested a gradual rebalance to strategic allocations should be initiated. We did precisely that in our PMS portfolios, reducing our cash position from 22% in the multi cap fund to 11%, with 5% being added at the market bottom and the remaining 6% early last week. Our view remains the same, with the emergence of re-assuring macro data on crude, earnings, and trade war.

India to Stand Out on Growth

Some Asian economies have joined developed economies in seeing weak macroeconomics. Taiwan, Thailand and Malaysia have slipped into contraction. European countries are losing momentum, with Italy and Germany slowing. While the global economic expansion story could lose steam, with China stalling, India’s growth looks healthy.

Emerging Markets Look Set to Outperform

As we had also discussed, the elections prompted a rotation back to EM assets. Emerging market stock buying surged to its highest levels since February post the U.S. midterm elections. Financial flow data showed that fund managers poured $3.9 billion into emerging equities, and $3.2 billion poured into EM debt.

Macro Positives and Earnings Growth Remain Healthy

Should crude continue to maintain current levels, this bodes well for current quarter earnings recovery. Valuations are hovering near reasonable value. The drop in Crude is going to help India in all manner of ways, from CAD to currency to consumer and business. The freeze in the NBFC space is alleviating and a respected fund manager we spoke to feels we are at about 70-80% of prior market activity.

A Turn in PMI Data Provides Further Comfort

The global slowdown does not appear to be devolving; meanwhile, India is growing credit at double digits and earnings at double digits. The most recent PMI data showed an uptick and further supports the view that the Indian economy is healthy and holding its own. Just as important, domestic flows remain strong and should the current macro scenario stabilize, a fair bit of cash will be looking to enter equities in coming weeks.

We continue to recommend that investors that have seen their equity allocations trimmed due to the sell-off gradually rebalance to strategic asset allocation. The market is oftentimes, a good leading indicator, and the market is telling us that things aren’t as bad as participants believe.

Fixed Income

The drop in crude oil and the muted inflation data led to duration funds delivering strong returns in the past month, as the 10 year fell to 7.78. The FI buyer returned for the first time in months. The Trump loss in the House derails the Republican agenda and the U.S. growth story now looks set to take a back seat to emerging markets.

Yields also benefitted as the NBFC funding crisis has stabilized, and due to the government’s reduced borrowing by 70k crore. Over the rolling three months, the RBI has also conducted OMOs around Rs 1 lakh crores, with INR 40k crore slated for November.

With the dramatically shifting currents, and macros, there is limited visibility to consider duration. Bond fund managers expect election surprises or macro events could easily create volatility in prices, so the prudent choice is to avoid duration. On the other hand, the decline in crude and muted inflation suggest that the RBI will be on pause at the next meeting.

Wider systemic risk has been contained with assurances of liquidity support from the RBI, securities regulator and the finance ministry. Fears of a credit squeeze also appear to be abating, with the recent data on credit growth. NBFCs have started getting line up financing from banks and away from CPs, an additional healthy sign. Additional negative surprises, if any, are likely to be of a one-off nature.

It is difficult at this point to prefer a particular category. Credit risk funds carry their share of uncertainty in terms of paper quality, which will get repriced in coming days. Corporate bond funds have disappointed from a returns perspective year to date. In the current scenario, structured products that deliver bond type returns with equity upside, remain particularly attractive. Manager selection will be an additional critical return determinant. Diversification across categories, FMPs and standalone high-quality credit paper remain preferred investment choices.

Technical Strategy

The Diwali truncated week saw equity markets trading in a narrow range of 142 points as market participants avoided heavy positions due to holidays. On Friday index opened in the positive but failed sustain above 10600 levels. For the week the Nifty closed marginally higher by 0.3% at 10585 levels. Broader market indices BSE Midcap and SmallCap gained 1.4% and 0.4% for the week. The bounce back from 26th October low of 10030 index formed a bullish long candlestick on weekly chart and now formed small body candlestick for last week. Thus, suggesting pause in the rally and consolidation at current levels. Now, immediate support is seen at 10440 levels; breaking below this decline towards 10340 and then 10260 can be seen. On the upside index needs to cross and sustain above 10600 for the bounce back to continue to towards 10750-10850 levels. Here couple of resistances are seen, the 200-day moving average which comes around 10762 levels and 4th October falling gap area of 10750-10850 levels will act as resistance for the market. In Nifty options, maximum open interest for Puts is seen at strike price 10000 followed by 10200; for Calls it is seen at strike price 11000 followed by 10800 and 10700. Some Call writing was seen in 11000, 10800 and 10700 while Put writing was seen 10100. India VIX closed at 17.77 down by 2.6% for the week. VIX has seen has seen cooling off from two and half year and further decline below 17 help in sustainable bounce back. However, rise in volatility will lead to resumption of decline in the market.