Sep 16, 2019

“The older I get, the more I see a straight path where I want to go. If you’re going to hunt elephants, don’t get off the trail for a rabbit.” – T Boone Pickens

This week we update our quarterly RICS asset pairs methodology.

Equities Vs Bonds

While acknowledging that forward earnings can be like a mirage in the desert, the forward earnings yield differential between bonds and equities has moved to levels historically associated with attractive returns for equities. On a trailing basis, the measure remains in neutral territory.

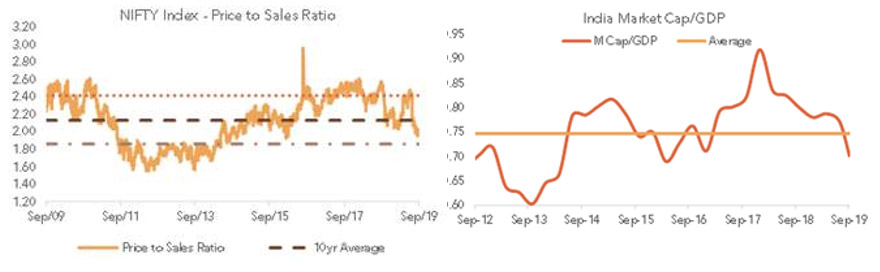

The trailing Price to Sales ratio is a purer approach based on top line, and is also approaching levels historically associated with attractive equity environments, at roughly a standard deviation below the 10 year average. As discussed, the challenge for most firms has been managing rising interest costs and credit liquidity efficiently enough to translate top line to profit delivery. Finally, market cap to GDP has also shrunk below the historical averages, reflecting the massive damage that has been inflicted on the broader market. As a result, our RICS asset pairs signal for equities moves to Neutral between equities and bonds, from a slight negative for equities score last quarter.

The Forward Equity Bond Yield Differential is Signaling an Attractive Environment for Equities…

…and the India Premium Over MSCI Emerging Markets is Back to Long Term Averages

The Price to Sales Ratio and Market Cap/GDP Also Signal Attractiveness for Equities…

Large Cap Vs Mid Cap

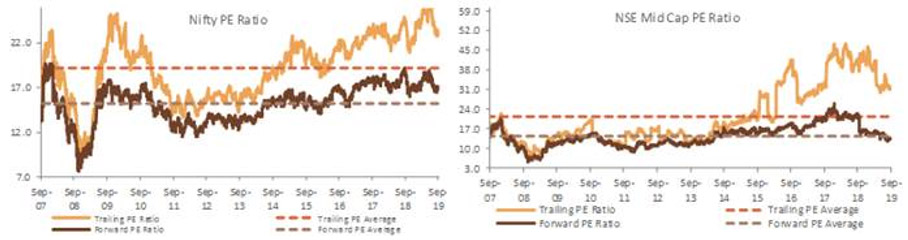

Equity research analysts appear to be finding cheer at mid cap companies, that isn’t readily apparent to the macro investor community. The forward P/E ratio for mid caps has declined below its long term average, while the forward P/E ratio for large caps remains above its average.

Revisions Data Favor Mid Caps

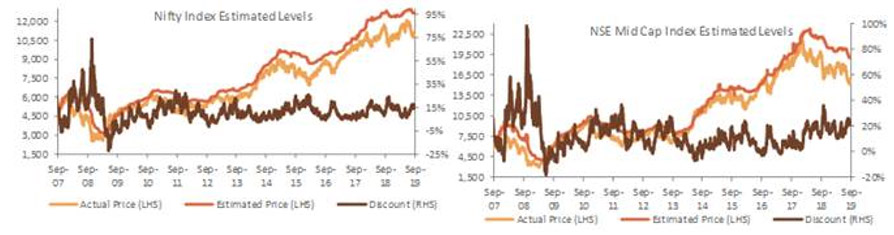

Further, the eps revisions data demonstrates an uptrend since late last year in midcap earnings revisions, while revisions for the Nifty 50 remain largely static. Mid caps appear to be witnessing improving momentum relative to large caps. Finally, the discount to analyst estimated levels is marginally higher for mid caps relative to large caps.

The Mid Cap Forward PE Ratios are Back to Long Term Averages, Lower than Nifty P/E Ratios…

…However, Let’s Remember that Forward Earnings Are Notoriously Illusive

The Forward Equity Bond Yield Differential is Signaling an Attractive Environment for Equities…

The Forward Equity Bond Yield Differential is Signaling an Attractive Environment for Equities…

Sanctum Asset Pair Model Recommends a Minor Tilt to Mid Caps over Large Caps

Our asset pair comparison suggests a minor overweight to mid caps. We temper our recommendation by noting that the price action has not yet demonstrated any beginning of an outperforming move in midcaps. Also, we note that forward earnings can often be a chimera, and the basis of our change in recommendation is on forward earnings and earnings revisions. Normally, we have found it prudent to follow the market, not lead it. Therefore, we’d be conservative in the allocation tilt towards mid caps, and stagger allocations over a period of time.

Recommendation: Multi Cap Fund Titans

One way to achieve a tilt is by increasing exposure to multi cap funds. Our in-house multi cap fund now sports a P/E of 23.5 times FY20, lower than the market despite delivering consistent 16-18% earnings growth. During the recently concluded quarter, as well, Titans portfolio delivered 15.2% earnings growth, compared with mid single digits for the Nifty 50. Titans has outperformed its benchmark (NSE 200) by 7.4% over the past six months, and 5.2% YTD.

Mid Cap Underperformance Continues With No Sign of a Relative Improvement

>Corporate Bonds Vs G-Secs

The spread between the 10 year g-sec yield and the repo rate has compressed meaningfully. However, the spread between corporate bonds and g-secs has widened over the past few weeks, as the government bond has moved lower tracking short term rates. Corporate bond yields have moved lower, but by less, therefore leading to spreads increasing to historically high levels.

The spread between g-sec yields and AAA yields remains consistent across the short and long end of the curve. Therefore, there is no advantage that appears evident on the short or long end.

The Spread Between the G-Sec and Corporate Bonds Has Widened to Above Average Levels

While the Repo Rate to 10 Year G-Sec Spread Has Narrowed…

…G-Sec Vs AAA Spreads Remain Wide Across the Yield Curve

>Corporates Have Not Tracked G-Secs Lower One for One

The inability of corporates to track govt yields lower could be the consistent, negative news flow, with Altico being the latest default announcement. Further exacerbating the situation, CRISIL has downgraded the highest number of corporates since Q3 2017, and the upgrade downgrade ratio is now notably negative for the first time since Q3 2017. These downgrades feel about a year late from our perch. The pairs model was positive on corporate bonds and now squarely at Neutral between corporates and g-secs.

CRISIL Downgrades Have Picked Up Meaningfully As They Did in Q2 and Q3 2017 …

…Meanwhile, the India U.S. 10 Year Spread Remains Barely Below the Long Term Average at 498 bps

USD Vs Rupee

FI flows into equities appear to have bottomed, and FI flows into debt remain healthy. FDI flows remain strong. However, the crude oil price spike is a negative for INR. While forex reserves remain healthy, and the import cover has improved of late, the biggest risk remains movements and geo-political risks emanating out of the Middle East. Therefore, while our model has a Neutral rating, it does not reflect the recent Saudi attack news, and we would be watchful for any negative impacts of rising crude on the Rupee, i.e., a Weakening of the Rupee. Should there be a sharp move, we’d expect the RBI to come in and engage in stabilizing measures.

Gold

With stimulus by the ECB, essentially the central bank is all in. Gold saw this before investors did, and likely reflects the news already. Gold has witnessed a clean breakout across fundamental and technical metrics. With further QE likely in coming months, Gold deserves an allocation in investor portfolios. Our RICS model has moved from a negative rating on Gold last quarter to a positive +1 score, signalling an overweight on Gold relative to cash.

Gold Rising Despite a Rising Trade Weighted Dollar…

…The Gold to Copper Ratio Signals a Weak Global Environment and QE

Outlook

Equities

Crude Oil Risks

On to the big news this weekend. The coordinated 10 drone strike on Saudi oil Aramco facilities is being linked to Houti rebels, backed by Iran. Consider it retribution for U.S. sanctions on Iran and Iran becoming increasingly belligerent with regard to Saudi’s actions. Many months ago, we had written about the need for our government to make crude import a matter of national security and stability, and consider hedging the acquisition price of oil. Certain latin American countries do this. The news this weekend presents a risk to India’s economy and nascent recovery, and leaves the economy captive and vulnerable to external shocks.

Crude oil could spike higher in the short term. This could add pressure on the fiscal, if the move is sustained in nature. Moves of this nature generally tend to be short term in nature, and self-correcting, but can inflict meaningful damage on markets if prevailing sentiment is negative. With a less hawkish administration in the White House, the likelihood of a dramatic Saudi retaliation looks unlikely. More likely, this was aimed at reducing the attractiveness of the Aramco IPO. The move higher in crude oil ironically benefits both Iran and Saudi.

ECB: However Long It Takes

The ECB has gone all in as chief Mario Draghi pledged indefinite stimulus last week to revive an ailing euro zone economy. The ECB cut rates deeper into negative territory and promised bond purchases with no end-date to push borrowing costs even lower. That was the primary reason behind global market stability in recent days.

Finance Ministry Measures for Housing and Exports

Finance Minister Nirmala Sitharaman announced measures over the weekend to boost housing and export sectors, with the highlight being a ₹10,000 crore special window to extend funding to net worth positive, incomplete housing projects. Measures are also being taken to improve credit outflows from banks, and transmission of interest rate cuts. Further, input tax credit refunds for exporters will be speeded up.

Equities

Domestic Recovery Underway but Crude Oil Uncertainty

Just as we were beginning to wonder if investors are adequately positioned domestically for positive economic news flow, the attack on the Saudi fields brings crude back into the equation. Oil importers are likely to be affected, as are companies with raw material imports, and oil derivative imports. Should the move on crude sustain, margins are likely to be impacted, yet again for sections of the market. The weakness in the Rupee should it unfold would be immediately attractive for IT, pharma.

Our RICS model has moved from slightly underweight equities to Neutral equities relative to bonds, and the directionality is towards equities.

Our views on equities remain unchanged, except that the risks in the short term now appear elevated with respect to crude. It is difficult to get a handle on the potential impact and bears monitoring, but we expect the situation to self-correct in coming days/weeks.

Portfolios constructed to deal with multiple outcomes rather than a specific view remain preferable. These would include quality growth, capital protected strategies, long short, Gold and Silver, global diversification, and tactical hedging.

Fixed Income

A spike in the price of crude could impact yields in the short term, adding to fiscal pressures for an already fiscally constrained government. In the short term, the impact is likely to be absorbed by international oil reserves; should the situation remain unresolved for an extended length of time, the impact to the global economy could be tangible.

While a rate cut was widely expected by the RBI at their next meeting in early October, crude now throws a bit of a monkey wrench into that calculus.

A diversified portfolio of AAA rated, highest quality, corporate bonds, banking and PSU bond funds, short, medium term bonds, low to moderate duration remains our preferred positioning. Fresh money allocations would be best advised post the stabilisation of the situation in Saudi Arabia.

Technical Outlook

The Nifty closed at 11,076 up by 1.18% for the week. It was a strong ending with Nifty closing near the highs on Friday and for week. Broader market indices BSE Midcap and Smallcap outperformed the benchmark with 2.25% and 3.32% gains respectively on weekly basis. Nifty has seen good bounce back after recent low of 10,746. It has bullish inverted head and shoulders pattern and the neckline for same is seen at 11,150 odd levels. The index has resistance zone around 11,150-11,225 where recent highs, 200 day moving average and 38.2% Fibonacci retracement of the fall 12,103-10,637 are seen. Thus, 11,225 is the breakout level which needs to be taken out for uptrend to continue initially towards 11,370 and then 11,543 levels. On downside immediate support is seen at 10,946 levels, breaking below which profit booking can be seen towards 10,850 and 10,746 levels. In Nifty September monthly expiry options, maximum open interest for Put is seen at strike price 10,800 followed by 11,000; while for Call maximum open interest is seen at 11,200 followed by 11,300. Nifty Put-Call option distribution data is suggesting is support at 10,800 levels and resistance at 11,200 levels. India VIX declined by 8.42% to close at 14.90 levels for the week. VIX after trading in a range of 18.5-16 is moving lower which should support the market in sustainable bounce back. However, VIX moving back above 16 will the cap upside for the market.