Apr 1, 2019

“Financial markets do not play a purely passive role; they can also affect the so-called fundamentals they are supposed to reflect. These two functions, that financial markets perform, work in opposite directions. In the passive or cognitive function, the fundamentals are supposed to determine market prices. In the active or manipulative function market, prices find ways of influencing the fundamentals. When both functions operate at the same time, they interfere with each other. The supposedly independent variable of one function is the dependent variable of the other, so that neither function has a truly independent variable. As a result, neither market prices nor the underlying reality is fully determined. Both suffer from an element of uncertainty that cannot be quantified.”– George Soros

Before we get to financial market commentary, a brief recap of the quarter gone by…

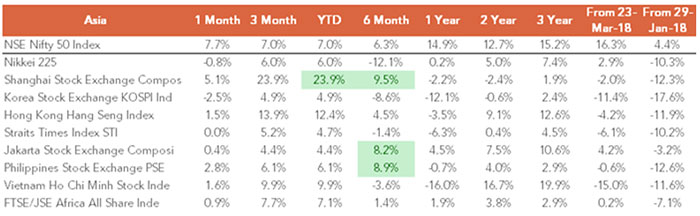

The S&P 500 Rose 12.3%, Outperforming the Nifty 50’s 7.0% YTD Return…

…But Underperforming the Nifty 50 by 8.2% over the Past Year

Chinese Stocks Were Top Performers for the Quarter, +23.9%…

…But India Has Outperformed All Major Asian EMs Over the Past Year, 2 Years and 3 Years

The Star Performer This Quarter Was NYMEX Crude, Up 29.3%

Despite Yield Curve Shenanigans, Gold Has Not Caught a Bid…

…While Copper’s Rise is a Good Sign for the Global Economy

Commodities Picked Up During Q1, Driven Largely by Optimism on China Stimulus and Trade…

…But Remain in Deflationary Trends Longer Term

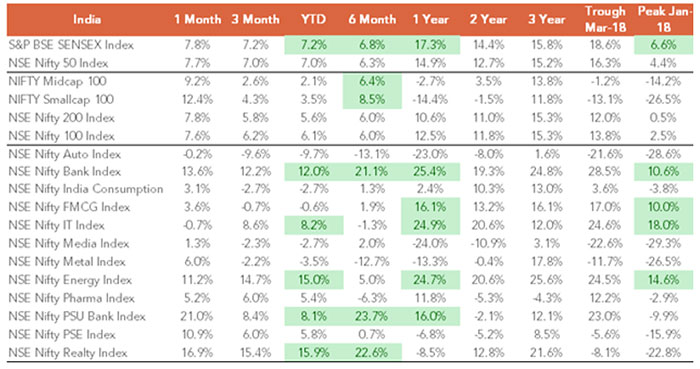

Domestic Equities Have Delivered 15.8% CAGR Over 3 Years…

…The Nifty 50 (+7.0%) outperformed Mid (+2.1%) and Small Caps (+3.5%) YTD…

…and the Nifty (+14.9%) Trounced Mid (-2.7%) and Small Caps (-14.4%) over the Past1 Year…

Sectorally, Banks, FMCG, IT and Energy Were Top Performers

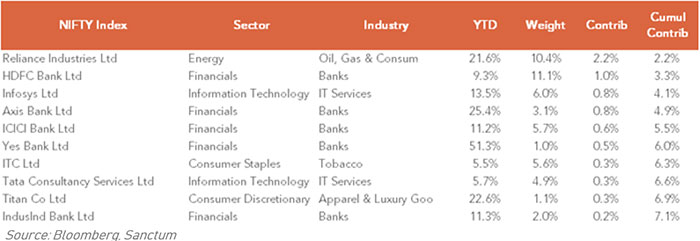

Top Contributors to the Nifty 50’s 1 Year Return – Reliance, HDFC, ICICI, Infosys & TCS…

Top Contributors Year to Date Are the Usual Suspects…

…With Axis Bank and ICICI As New Entrants

Investment Commentary

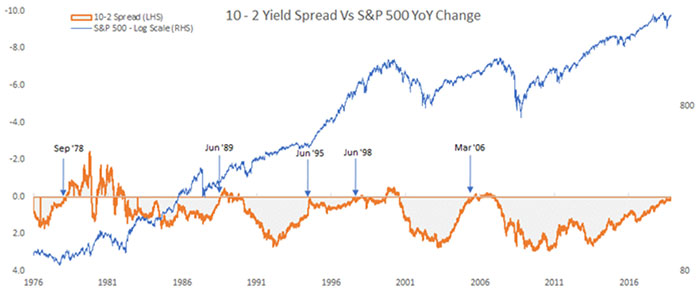

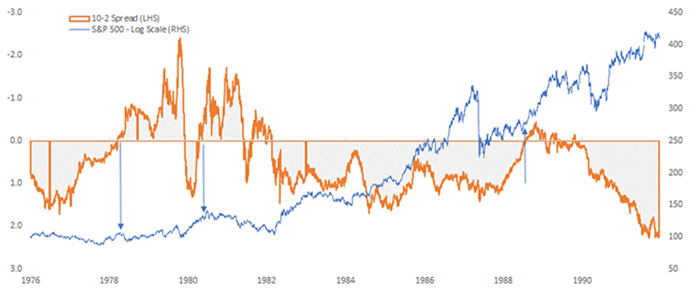

The Global Business Cycle Reached a Significant Milestone This Week with Yield Curve Inversion

The yield curve has been an accurate predictor of recessions in the U.S. for decades, and one must acknowledge the historical accuracy of the signal. The most recent inversion was in March 2006, a lead time of 21 months to the eventual peak in Nov 2007.

Prior to that, the spread inverted in Jun 1998, preceding the Long Term Capital Management crisis and the Nasdaq Bubble, a lead time of 21 months. Looking further back, there was a close call in Jun 1995, but that signal reversed. The prior signal was Jun 1989, and that pre-empted the Gulf War recession.

An Inverted Yield Curve Is at the Simplest, Usually About the Fed Raising Rates Too Far

The simplest reason for the yield curve inversions is usually the Fed raises short rates too high. Should the Fed act aggressively now and reverse the rate increases, we could follow the template set in 1995. However, there are other indicators besides the yield curve signalling slowing growth in the U.S., and worryingly, corporate commentary by global economy corporates such as Fedex are of particular concern.

Separately, the creator of the yield curve inversion indicator stated that the curve must be inverted for three months for a signal to take effect, so there is that factor to keep in mind.

Developed Economies Are Back to Square One

The global developed economy is back to square one, with global markets expecting synchronized stimulus and rate cuts. Federal Reserve officials have slashed their projected interest-rate increases this year to zero from two, and the ECB has extended its pledge to keep rates low. Policy makers in China are working on fiscal and monetary stimulus to revive growth. The global economy increases resembles a one trick pony (stimulus) again, unable to generate either inflation or growth, running on the fading fumes of QE, negative interest rates, tax stimulus and corporate buybacks.

As such, the accommodative stance of central bankers is the primary catalyst for the multi-asset gains witnessed year to date 2019. Investors are yet again putting aside their misgivings about central bank excesses and buying.

The Yield Curve’s Track Record is Long Lead in Nature, Not Perfect But Not to be Discounted

Drilling Deeper, There Have Been False Signals and Markets Have Generally Been Able to Stay Above Signal Levels

…Additional Signals in 1994, 1998 and 2005 Again Demonstrate the Difficulty of Timing the Curve

Decoding the Developed Economy Debt Albatross

Today, around $10 trillion of bonds are trading at negative yields, mainly in Europe and Japan. In the next recession, U.S. interest rates, too, will likely approach negative territory, since cuts of 3% are normally required to restart economic activity, and short rates in the U.S. are currently at 2.5%. Negative rates are telling us that the global economic system cannot generate sufficient income to service current debt levels at normalized rates. Artificially depressed rates are necessary for debt to be barely managed.

Unintended Consequences – Savers Lose

The world is in this predicament due to the failure to deal with unsustainable debt levels. The only feasible strategy, the one that the Fed hoped for is to reduce debt via growth and/or inflation. Neither appears to be coming forward. Default is clearly not an option. Therefore, central banks are forced to use low rates to manage excessive debt levels. The unintended consequence is a transference of wealth from savers to borrowers through the gradual degradation of real purchasing power and standard of living. Rates are unlikely to normalize for years to come. The solution for savers facing such threat of losses is to increase investment, but the lost decade of the 2000s in the U.S. makes that a very difficult ask.

Domestic Economy

Musing the future prospects of developed economies is most certainly not a pleasant exercise and the Indian economy by relative contrast is a refreshing breath of fresh air. Our problems seem relatively more manageable, and we have the one factor that’s so desperately missing in the developed world – growth.

Unfolding Along Expected Lines…Asia’s Contribution to Growth at 63%, China, India Indonesia Key

Asia as a whole now accounts for 63% of all global GDP growth (PPP), with the lion’s share going to China, India and Indonesia, while Japan will only contribute 1% to the global growth. In the past 40 years, developing Asia has increased its share of the global economy (in PPP terms) from 8.9% to an estimated 34.1% today. This dominant region includes China, India, and other fast-growing economies. By contrast, the European Union and the United States combined for 51.5% of global productivity in 1980, and now account for 31%.

Unfolding as Expected…Developing Asia’s Share of Global Growth Has Risen to 34.1%…

While Euro, U.S. are Now Down to 31%

Outlook

Equities

Despite Dismal Global Dynamics this Past Decade, the Nifty 50 Has Delivered 85% Over 5 years

Focusing on global worries can be harmful for portfolios and cause investors to make mistakes that result in significant lost opportunity. Five years ago, the Nifty PE rose above 20 times, there were worries about China debt, the U.S. business cycle, Brexit, Italy, demonetization, PSU NPAs etc etc. Yet the PE has persistently stayed elevated, and the Nifty 50 has delivered an 85% total return during the past five years, call it 16% CAGR, far surpassing returns from alternative classes.

Macros Remain in Place for Equities with Positive Real Yields, Low Inflation and Rate Cuts

Clearly, skeptics will argue that the move has been driven by valuation expansion and limited earnings growth. That is a valid point at the index level. But valuations have stayed elevated on visible long-term growth, structural reforms, and declining inflation. With low inflation, real yields are attractive and will sustain markets alongside low inflation and rate cuts.

DII selling at 3-year high in March and the Largest Share of FII Flows to India

Domestic institutional managers sold 12,800 crores in equities in March, the highest in three years. February saw inflows into equity schemes of 5,100 crores, lowest in 25 months. Monthly contributions through SIPs remain steady at 8,000 crores. Meanwhile, FIs bought 25,000 crores in March, the highest inflow since March 2017. Notably, India received the largest share of FII inflows (ex China) according to data compiled by Goldman Sachs.

Back to the Future

Clearly, the yield curve inversion brings good and bad news. The good news is central bank liquidity. The bad news is slowing global growth and a possible recession. We’re Back to the Future, with central bankers the caretakers of a sluggish, QE addicted global economy.

Accommodative Policy a Core Part of the Backdrop

Despite a five year period racked with worrisome fundamentals, Indian equities have delivered 16% CAGR. With strong multi-billion dollar commitments by foreign investors, it is likely the market hits new highs. Should the incumbent party win, significant domestic capital is likely to further flood the market.

Timely rate cuts globally, and domestically, now form the core backdrop. A stable party election verdict is the odds on outcome and continues to favor our positive stance on the markets.

Debt Outlook

$2 Billion FPI Capital Finds its Way into Debt in March 2019

As a result of what now looks like a fairly stable currency, dovish Fed commentary, the impending release of global liquidity, a $5 billion dollar swap to boost domestic liquidity, voluntary retention regulations beneficial to FPIs, and a rising spread between U.S. and G-sec bond yields currently at 495bps, foreign portfolio investors (FPIs) turned net buyers of Indian bonds. Bond yields had peaked in Sep ’18 at 8.13% and have now declined to 7.34%. Foreign investors bought bonds to the tune of $2.03 billion in March alone, clocking the biggest monthly buy since October 2017.

A Case for Gilts for Moderate and Aggressive Asset Allocation Profiles

We recognize gilts are volatile bond investments with potential for capital loss, particularly given the challenges of a three-year investment horizon. In particular, this advice does not apply to debt income investors seeking regular income that have a stated aversion to capital losses, nor is it an interest rate forecast; rather, it is an asset allocation and portfolio optimization strategy worth considering in light of the signals emanating from the global economy.

For moderate and aggressive asset allocation portfolios, it is time to acknowledge yield inversion and the possibility of a recession in the U.S., and tune portfolios accordingly in coming weeks, adding a highly negatively correlated investment stream to buttress diversified portfolios during sharp downturns.

Long term gilt funds historically provide high positive returns during sharp down years. Gilts delivered 28.5% in 2008, 12.1% in 2012, and 15.9% in 2016, and an annualized 10.9% over the past year, outperforming all debt categories. Over longer periods, gild funds have fared well. The five-year rolling returns of gilt funds for the past seven years are higher than that of other debt fund categories. In what has been referred to by academics as the only “free lunch” in investing, diversifying investment portfolios with negative correlation assets such as Gilts leads to higher risk adjusted portfolio returns.

It is likely that the RBI will be cutting rates by 50 bps in coming days and weeks. With inflation muted, globally and domestically, high real yields, an accommodative Fed, and a slowing economy, a fair number of forces are exacting downward pressure on rates. Given their allocation to sovereign bonds, gilt funds are generally immune to default risk and credit rating downgrades. Gilts do bring in a measure of volatility. Therefore, an appropriately structured allocation should be considered. For safety from manager intervention, 10 year constant maturity gilt funds are an attractive option.

Much Pain for Limited Gain

Separately, debt investors have had to suffer an inordinate amount of capital loss risk in recent months, and in some cases write-downs, what with NBFCs ALM, stressed housing finance, developer funding, IL&FS, Dewan Housing, Indiabulls, SPVs, Holding Company, Promoter pledges etc. Return of capital has been garnering far greater mind share than is comfortable for most debt investors.

Credit Risk and Yield Compression

The 10 year AAA traded at 8.92% in September when Gilts traded at 8.13%, a spread of 83 bps. Today, the spread has widened to 117 bps, a widening of 35 bps, as corporate bonds have not benefitted to the same extent as interest rates softened. Further, a fair amount of paper has in fact had to be written down.

It’s clear that lenders were making loans with limited cover, priced for good times. Much of these practices stand exposed today. NBFC conglomerates grew their loan book at a rapid pace. Asset quality concerns remain, and stress within housing finance and real estate remain. Until the leverage unwinds, credit thaws, and mark to market normalizes, we’d avoid credit risk. Investors seeking capital preservation first and foremost would be well advised to stay in ultra-short and high quality until clarity emerges on stressed sectors, while those seeking higher yields can consider exposure to high quality corporate bonds of low to moderate duration.

Technical Outlook

Markets finished the final trading day of the financial year in positive to close at 11,623.9 with a gain of 0.47% for the day and 1.46% for the week. For FY19, Nifty saw gains of 14.93%. The broader market indices BSE Midcap and Smallcap gained 2.67% and 1.86%, respectively for the week outperforming the benchmark index.

Market breadth on NSE was positive with 5 stocks advancing for every 4 declines. Nifty has formed a long body bullish candlestick on weekly and monthly charts. Strong momentum suggests market is going to head towards its all-time high of 11,760. Immediate support of 11,550 needs to hold for last week’s rally to continue towards new highs.

Crossing and sustaining above 11,760 on tradable basis, the next level for Nifty is seen at 11,830 and 11,900. On the downside, last week’s low of 11,311 becomes critical support for the market. A decline below last week’s low would break the sequence of higher highs and higher lows. In Nifty options, maximum open interest for Puts is seen at strike price 11,500 followed by 11,000; while for Calls it is seen at strike price 12,000 and 11,600. Put writing was seen in 11,500 and 11,600 along with Call writing in 12,000 and 11,700. India VIX increased by 5.6% for the week to close at 17.2. In last three weeks volatility risen from 15 to current levels. VIX needs to settle at current level or decrease for rally to continue, otherwise further increase may stall market rally.